Source: New Luban

Despite experiencing rapid growth of 20-30% over two decades, China’s construction industry has consistently struggled with low profit margins. This persistent issue raises serious concerns among industry professionals and entrepreneurs alike. What factors contribute to these prolonged low profits, and what strategies can reverse this trend?

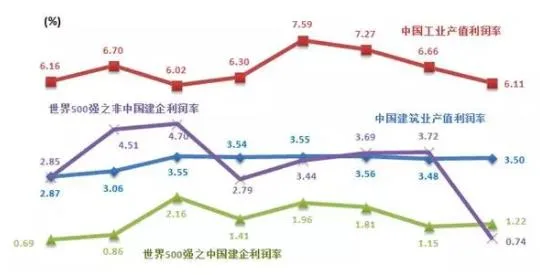

The long-standing low profitability of China’s construction sector is reflected clearly in several key data points:

Figure 1-4: Profit Rate Comparison Across Various Enterprise Types

Note: In 2013, the profit margin of Chinese construction companies listed in the Fortune Global 500 dropped to 0.74%, largely due to a 4.9% loss by ACS in Spain. Excluding ACS Group, several overseas construction firms maintained a profit margin of approximately 3.10%.

The chart reveals that China’s largest construction firms lag significantly behind their international counterparts in profitability and also trail the broader Chinese industrial average. Compared to other sectors, construction ranks as one of the lowest in profit margins within China.

Interestingly, this low profitability has persisted even as the construction industry’s growth rate has been two to three times faster than China’s GDP—contradicting typical economic laws. Furthermore, despite fierce competition and rapid industry expansion, the number of top-tier firms has increased rather than decreased, with few bankruptcies or mergers in recent years.

This scenario threatens the industry’s healthy development. Industry players and associations have urged local governments and regulators to revise bidding policies—favoring quota pricing over the current list quotation or “reasonable low price bidding.” The Ministry of Housing and Urban-Rural Development has introduced new “Special Qualification Standards for Construction General Contracting” to limit the number of general contractors and curb cutthroat competition. However, the effectiveness of these policy changes remains uncertain.

Identifying the Problem

Industry experts and entrepreneurs largely attribute the problem to two main factors: overcapacity and outdated production practices. Overcapacity suppresses prices and fuels vicious competition among construction firms. Outdated methods involve excessive profit-sharing among owners, designers, and other stakeholders, leaving minimal margins for the construction units themselves. Many call on the government to reform the current system.

Yet, attempts to control competition or adjust profit distribution often overlook the fundamental relationship between industry development and government policies.

Despite years of advocacy, the industry’s situation has not improved as expected. Instead, enterprise numbers and competition intensity have increased, while shifts toward modern contracting methods like engineering procurement and construction (EPC) remain limited.

To truly address the issue, it’s essential to dig deeper beneath the surface and explore viable solutions.

Globally, the trend is moving toward a low-carbon economy, primarily driven by private investment. In this context, winning contracts through the lowest bids—building quality projects with minimal resource consumption—has become standard practice. Government-funded projects internationally have long adopted lowest-price bidding. Thus, industry leaders must rethink how to thrive in this environment.

Relying on government intervention to improve the industry environment has proven naive, as past decade’s experience shows. Instead, enterprises should focus on internal transformation. Research by Luban Consulting indicates that internal reforms and management upgrades within companies offer the best chance to overcome difficulties and revitalize the industry.

The current industry dilemma stems mainly from stagnation in enterprise transformation and management improvements, influenced by outdated business concepts, fixed pricing methods, and remnants of planned economy thinking.

Uncovering the Truth

The construction sector is inherently high-risk—both legally (due to compliance issues) and operationally (cost, quality, and safety risks)—making its low profit margins all the more unreasonable.

On one hand, complaints about low profits abound; on the other, new entrants flood the market, with dozens or even hundreds of companies bidding for single projects. This paradox—low profits amid severe overcapacity and rapid growth—defies typical market logic. What explains this contradiction?

Truth 1: Low Corporate Profits, High Project Profits

Industry-wide low profits often refer only to the corporate headquarters, while individual projects may, in fact, generate substantial profits.

Due to outdated management systems, many Chinese construction firms—both private and state-owned—focus on project contracting to expand volume and geographical reach. This extensive operational model means profits largely remain at the project level. Corporate headquarters often act merely as “tax collectors,” earning minimal management fees or relying on internal financial mechanisms, while some firms depend on associated bidding to generate revenue.

Projects bear full responsibility for financing, quality, safety, and scheduling, while headquarters typically receive only 1-3% in management fees per project. Sometimes projects even absorb losses, with project managers abandoning failing contracts. Under these circumstances, low corporate profits alongside relatively high project-level profits are normal.

Truth 2: Low Profits at Corporate and Project Levels; High Profits for Individuals and Subcontractors

Another common scenario is where companies and projects show poor profitability, but individuals responsible for projects (such as contractors and procurement managers) and subcontractors earn significant profits.

This is especially prevalent in large state-owned firms and numerous private companies. Profit leaks occur due to weak cost control at both headquarters and project levels. Without effective oversight, project leaders may prioritize personal gain, diverting resources to subcontractors and suppliers, resulting in project losses.

Truth 3: General Contractors Have Low Profits; Specialized Firms Earn More

Despite widespread low industry profits, different market segments vary considerably (see table below):

Table 1-1: Operational Data of Various Construction Enterprise Types

Specialized companies enjoy profit margins 2-3 times higher than general contractors, with price-to-earnings (P/E) ratios 2-5 times greater, indicating stronger profitability and market recognition. Yet, many enterprises remain focused on expansion and diversification rather than strengthening core businesses or building strong brands, leading to persistently low profits.

The general contracting sector features many firms lacking clear brand differentiation or unique competitive advantages. As a result, price competition dominates, and low-profit survival has become the industry norm.

Truth 4: Enterprises, Projects, Individuals, and Subcontractors All Have Low Profits—but This Is Not the Norm

Enterprises that fail to generate profits ultimately cannot survive long-term; they either dissolve, shift industries, or merge. Market forces naturally weed out unprofitable players, so this scenario is less concerning.

The real issue is the low profitability at the corporate level caused by industry complexity and outdated management. When profits are concentrated at the project, individual, and subcontractor levels, they are unlikely to be reinvested in technological advancement, talent development, or industry innovation—hampering sustainable growth.

Root Causes

While overcapacity leads to fierce competition and price suppression, this is only a surface symptom.

The underlying problem lies in the neglect of building internal core competitiveness, resulting in low industry barriers. New entrants easily join the market with minimal risk.

General contractors, influenced by planned economy mindsets and relational competition, have failed to strengthen their capabilities. They lack competitive advantages in branding, technology, capital management, procurement, and cost control. Moreover, diseconomies of scale persist: large firms face higher costs than smaller ones, who in turn are costlier than individual contractors. This environment allows new entrants with project connections but limited management experience to proliferate, exacerbating competition.

Industries typically advance by either building strong brands (e.g., Apple, luxury brands) or achieving cost advantages through economies of scale that consolidate outdated capacity and block new entrants—examples include home appliances and retail chains. Without either in China’s construction sector, overcapacity cannot be controlled.

In the early 1990s, construction companies enjoyed a golden era with advance payments of up to 30% and generous subsidies above fixed prices. Those days have passed. Market forces of supply and demand dictate prices and competition, and administrative regulations have limited influence.

Current advances and price suppression largely stem from market competition rather than “bad owners.” Attempts to regulate through government policies are often circumvented via shadow contracts, coordinated by construction companies themselves, undermining market principles. As long as agreements are legal and consensual, such practices are part of the market economy.

Therefore, the responsibility for improving competition lies primarily with construction enterprises, not government policy.

Some large construction entrepreneurs hold outdated views, believing high costs and burdens are inevitable for big firms. They overlook their responsibility to innovate and improve efficiency, maximizing social value with minimal resource use.

While large firms face challenges, they also enjoy advantages—bulk purchasing and more efficient capital operations, for example—that smaller firms cannot match. Entrepreneurs often magnify their weaknesses instead of leveraging these strengths through innovation. Tolerating persistent diseconomies of scale is unacceptable.

Internationally, the construction industry demonstrates economies of scale with a healthy ecosystem of few large enterprises and many specialized subcontractors, as seen in Japan, Europe, and the US.

Similarly, other Chinese industries have embraced scale advantages, such as the food industry, where large chain brands dominate.

Persistent diseconomies of scale indicate poor innovation and a failure of entrepreneurial responsibility in the Chinese construction sector. This industry consumes over 50% of global deforestation, steel, and cement usage, and contributes half of China’s carbon emissions—posing a serious threat to future generations and the planet.

Construction entrepreneurs must recognize that without resolving diseconomies of scale, overcapacity and destructive price competition will persist. Waiting for government intervention is futile; enterprises themselves must lead the way through self-driven improvement.

Another symptom of low industry profits is the uneven distribution along the industrial chain. Many complain that construction firms have been reduced to mere “material processors,” with owners and designers capturing the majority of profits despite construction units bearing most risks. They hope the government will rectify this.

Such complaints are futile and reflect planned economy thinking. In a market economy, profit distribution is governed by market forces, not government intervention.

Industry chain integration and expansion are enterprise responsibilities operating under market rules. Unless upstream sectors are administrative monopolies (which they are not in construction), profit sharing depends on enterprise strategy and capability. Many construction firms divert funds into real estate, hindering industry development.

Success stories like Golden Mantis in the decoration sector illustrate the power of industry integration. By acquiring top design firms, investing in industrialized factories, and developing advanced IT systems, they have created competitive barriers and improved efficiency without relying on government mandates.

Recent industry policies have increased administrative barriers, contrary to international trends and WTO principles. Strict qualification standards risk creating profit classes focused on fees rather than innovation, stifling progress.

Ultimately, upstream profit sharing depends not on system reforms but on enterprise capability and strategic vision. Current project management still struggles with quality, safety, cost control, branding, and financial capacity, limiting upstream expansion.

Research by Luban Consulting suggests construction project management margins could improve significantly, from 2% up to 12%. Yet, funds are often diverted into real estate and diversification rather than technology, R&D, or talent development. This imbalance weakens the industry’s foundation.

In summary, the construction industry remains trapped in a cycle of low profits and vicious competition, influenced by outdated mindsets and external dependency. It is time for self-liberation.

The Path Forward

China’s construction industry today resembles a “besieged city.”

Financially, more firms profit from ancillary sectors like real estate and hotels rather than reinvesting in core construction. Human resources are also shifting: experienced entrepreneurs and project managers leave, replaced by inexperienced individuals willing to take risks. This turnover exacerbates quality, safety, and corruption issues.

Industry innovation is often wasted on manipulating bidding processes rather than improving operational excellence. The exodus of top talent combined with an influx of low-level workers threatens long-term development.

How can the industry improve profits and promote healthy growth?

First, understand industry development laws and recognize core issues.

The construction industry must grasp how market economy principles apply. Currently, leaders focus on managing crises rather than strategic research. Genuine understanding is crucial to meaningful change.

Second, adopt correct corporate values and abandon outdated planned economy thinking.

Entrepreneurs must embrace innovation and reject dependence on external support. A “civilian spirit” philosophy—valuing diligence and innovative management—can yield average or above-average profits.

Waiting for government policies that favor real estate or diversification risks missing critical opportunities. The construction industry holds vast potential but requires clear-eyed self-reflection and internal skill development.

Third, strengthen internal capabilities, build core competitiveness, and raise industry barriers.

Overcapacity and brutal competition stem from low entry barriers. Enterprises must enhance brand strength, technology, quality, and cost control to block unqualified entrants.

Large firms need to overcome diseconomies of scale to reduce costs, eliminate inefficient smaller competitors, and foster a healthy industrial ecosystem. Practices like “affiliated contracting” and “internal project contracting” should be replaced with direct sales and transparent management.

Achieving economies of scale requires embracing informatization and quickly adopting technologies like Building Information Modeling (BIM). Senior leadership should prioritize management and information technology to enable intensive operations, boost competitiveness, and improve profit margins. This transformation is within reach.

Must log in before commenting!

Sign Up